From Debt Trap to Dream Trip: Customer Experiences with Tribal Loans

From Debt Trap to Dream Trip: Customer Experiences with Tribal Loans

Let’s face it, sometimes life throws you a curveball. You need a little extra cash, but your credit score is less than stellar. You’ve been turned down by traditional lenders, and you’re feeling stuck. Enter tribal loans, a seemingly unconventional solution that’s gaining traction. But are they a lifeline or a risky gamble?

We’re diving into the real-life experiences of individuals who’ve ventured into the world of tribal loans. We’ll explore the highs and lows, the successes and the struggles, to give you a clear picture of what to expect.

Related Articles: From Debt Trap to Dream Trip: Customer Experiences with Tribal Loans

- Stuck In A Credit Crunch? Tribal Loans Might Be Your Lifeline

- Cash-Strapped? Tribal Loans: A Lifeline Or A Trap?

- Cashing In: Navigating The World Of Indian Reservation Loans Online

- Stuck In A Credit Rut? Tribal Installment Loans Could Be Your Lifeline

- Can I Get A Tribal Loan If I’m On Disability? Navigating The Tricky Waters Of Tribal Lending

What are Tribal Loans?

Tribal loans are offered by lenders who are affiliated with Native American tribes. They operate on sovereign land, which allows them to avoid certain state regulations that apply to traditional lenders. This means they can offer loans with higher interest rates and less stringent credit requirements.

Why Do People Choose Tribal Loans?

The allure of tribal loans lies in their accessibility. They’re often a last resort for individuals with bad credit or those who need quick cash. Here are some common reasons people opt for tribal loans:

- Fast Approval: Tribal lenders often boast quick approval times, sometimes within a day or even hours. This can be a lifesaver when you need cash in a hurry.

- No Credit Check: Many tribal lenders don’t conduct traditional credit checks, making them an option for those with poor credit history.

- Flexible Loan Amounts: Tribal loans are available in varying amounts, catering to different financial needs.

The Success Stories

"It Saved My Business" – Sarah, Small Business Owner

Sarah, a single mom running a small bakery, found herself in a bind. Her equipment broke down, and she couldn’t afford the repairs. Traditional lenders wouldn’t touch her with a ten-foot pole, but a tribal loan came through. "It saved my business," Sarah says. "I was able to get the repairs done, and now I’m back on my feet."

"I Finally Took My Dream Trip" – Michael, Travel Enthusiast

Michael, a passionate traveler, had always dreamt of visiting the Galapagos Islands. But his credit score held him back. A tribal loan allowed him to finally make his dream a reality. "It was a once-in-a-lifetime experience," Michael says. "I wouldn’t have been able to do it without the loan."

"It Gave Me a Fresh Start" – Emily, Student Loan Debt

Emily was drowning in student loan debt. She was struggling to make ends meet, and her credit score was taking a hit. A tribal loan helped her consolidate her debt and get back on track. "It gave me a fresh start," Emily says. "I’m finally able to breathe a little easier."

The Challenges

While these stories offer a glimpse of hope, it’s crucial to acknowledge the potential pitfalls of tribal loans.

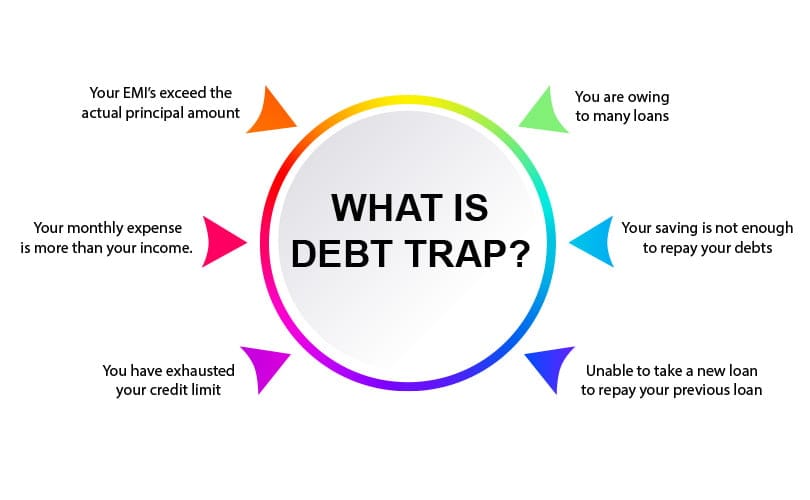

- High Interest Rates: Tribal loans often come with exorbitant interest rates, which can quickly spiral out of control if you’re not careful.

- Short Repayment Terms: The repayment terms for tribal loans are typically short, putting pressure on borrowers to make large payments.

- Aggressive Collection Practices: Some tribal lenders have been accused of using aggressive collection tactics, which can be stressful and damaging to borrowers.

Tips for Navigating Tribal Loans

If you’re considering a tribal loan, proceed with caution. Here are some tips to help you make an informed decision:

- Shop Around: Compare rates and terms from multiple lenders before committing to a loan.

- Read the Fine Print: Pay close attention to the interest rate, fees, and repayment terms before signing anything.

- Understand Your Budget: Make sure you can comfortably afford the monthly payments before taking out a loan.

- Consider Alternatives: Explore other options, such as personal loans, credit cards, or even asking friends or family for help, before resorting to tribal loans.

When Tribal Loans Might Be Right for You

Despite the risks, tribal loans can be a viable option in certain situations. Here are a few scenarios where they might be worth considering:

- Emergency Expenses: If you need cash quickly to cover an unexpected expense, such as a medical bill or car repair, a tribal loan might be a temporary solution.

- Limited Credit Options: If you have bad credit and are unable to secure traditional loans, a tribal loan might be your only option.

- Small Loan Amounts: If you only need a small amount of money, the high interest rates might not be as detrimental.

The Bottom Line

Tribal loans are a controversial topic. They can be a lifesaver for some, but they can also lead to financial hardship for others. If you’re considering a tribal loan, do your research, compare options, and proceed with caution.

FAQ

Q: What are the legal implications of tribal loans?

A: Tribal loans are a complex legal issue. They are regulated by tribal law, but they can also be subject to state and federal laws. It’s important to understand the legal framework surrounding tribal loans before taking one out.

Q: How can I find a reputable tribal lender?

A: Look for lenders that are members of the National Tribal Loan Association (NTLA). The NTLA promotes responsible lending practices and ethical behavior among tribal lenders.

Q: What are some alternatives to tribal loans?

A: There are many alternatives to tribal loans, including personal loans, credit cards, payday loans, and even asking friends or family for help. It’s important to compare options and choose the one that best fits your needs and financial situation.

Q: What are the risks associated with tribal loans?

A: The risks associated with tribal loans include high interest rates, short repayment terms, aggressive collection practices, and potential legal issues. It’s important to weigh the risks and benefits carefully before taking out a tribal loan.

Remember, before taking out any loan, it’s crucial to assess your financial situation, explore alternatives, and make an informed decision. Financial literacy is key to navigating the often-complex world of lending.

Closure

Thus, we hope this article has provided valuable insights into From Debt Trap to Dream Trip: Customer Experiences with Tribal Loans. We thank you for taking the time to read this article. See you in our next article!

")